Agreement between insurer and agent

FREE

Ask the similar questions

Agreement between insurer and agent

Insurer and Agent

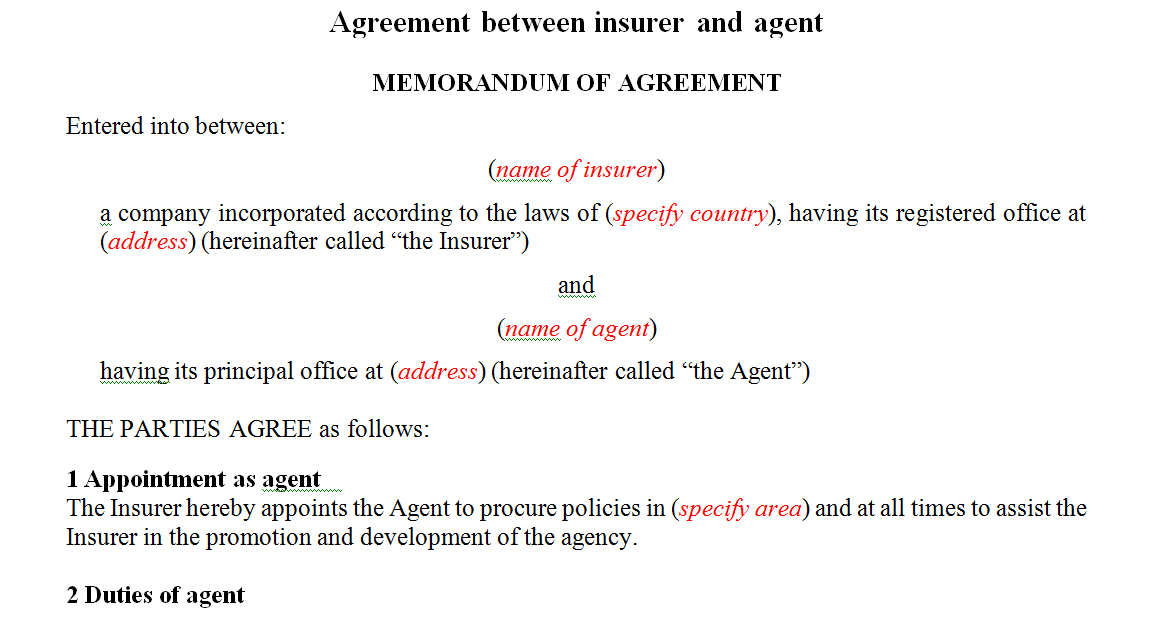

Agreement between the insurer and the agent setting out the details of the appointment of the agent, duties, documentation, remuneration etc.

Agreement between Insurer and Agent

This is a written contract stipulating the arrangement between an insurance agency and the insurer it represents. Important details such as ownership of renewals, commission percentages, and duties and responsibilities of each party are usually spelled out in this agreement.

Insurance agents have contractual agreements (known as Appointments) with insurers that set up the guidelines for the policies they can offer and the terms of their remuneration. A ‘captive agent’ is an agent dedicated to one insurance company’s product while an 'independent agent'can align themselves with multiple insurers. The insurance agent therefore aims to attract insurance business for their principal(s).

Insurance is sold primarily by agents. The underlying contract, therefore, is affected significantly by the legal authority of the agent, which in turn is determined by well-established general legal rules regarding agency. The law of agency basically deals with the legal consequences of people acting on behalf of other people or organizations.

Agency involves three parties: the principal, the agent, and a third party. The principal(insurer) creates an agency relationship with a second party by authorizing him or her to make contracts with third parties (policyholders) on the principal’s behalf. The second party to this relationship is known as the agent, who is authorized to make contracts with a third party. It is important to note the difference between an agent who represents the insurer and a broker who represents the insured. However, in certain instances brokers are not allowed to operate unless they also obtain an agency appointment with an insurer.

The source of the agent’s authority is the principal. Such authority may be either expressed or implied. When an agent is appointed, the principal is required to expressly indicate the extent of the agent’s authority in the agreement. The agent also has, by implication, whatever authority is needed to fulfil the purposes of the agency.

By entering into the relationship, the principal implies that the agent has the authority to fulfil the principal’s responsibilities, implying apparent authority. From the public’s point of view, the agent’s authority is whatever it appears to be.

If the principal treats a second party as if the person were an agent, then an agency is created. When entering to such agreements the parties should be aware that agency law and the doctrines of waiver and estoppel have serious implications in the insurance business.

Binding Authority

The law of agency is significant to insurance in large part because the only direct interaction most buyers of insurance have with the insurance company is through an agent or a broker, also called a producer. Laws regarding the authority and responsibility of an agent, therefore, affect the contractual relationship.

One of the most important agency characteristics is binding authority. In many situations, an agent is able to exercise binding authority, which secures (binds) coverage for an insured without any additional input from the insurer. The agreement that exists before a contract is issued is called a binder. This arrangement, described in the offer and acceptance section, is common in the property/casualty insurance areas. If you call an agent in the middle of the night to obtain insurance for your new motor vehicle, you are covered as of the time of your conversation with the agent.

In life and health insurance, an agent’s ability to secure coverage is generally more limited. Rather than issuing a general binder of coverage, some life insurance agents may be permitted to issue only a conditional binder. A conditional binder implies that coverage exists only if the underwriter ultimately accepts (or would have accepted) the application for insurance. Thus, if the applicant dies prior to the final policy issuance, payment is made if the applicant would have been acceptable to the insurer as an insured. The general binder, in contrast, provides coverage immediately, even if the applicant is later found to be an unacceptable policyholder and coverage is cancelled at that point.

Estoppel

Estoppel occurs when the insurer or its agent has led the insured into believing that coverage exists and, as a consequence, the insurer cannot later claim that no coverage existed. For example, when an insured specifically requests a certain kind of coverage when applying for insurance and is not told it is not available, that coverage likely exists, even if the policy wording states otherwise, because the agent implied such coverage at the time of sale, and the insurer is estopped from denying it.

Agency by Estoppel

An agency relationship may be created by estoppel when the conduct of the principal implies that an agency exists. In such a case, the principal will be estopped from denying the existence of the agency (recall the binding authority of some agents). This situation may arise when the company suspends an agent, but the agent retains possession of blank policies.

People who are not agents of a company do not have blank policies in their possession. By leaving them with the former agent, the company is acting as if he or she is a current agent. If the former agent issues those policies, the company is estopped from denying the existence of an agency relationship and will be bound by the policy.

If an agent who has been suspended sends business to the company that is accepted, the agency relationship will be ratified by such action and the company will be estopped from denying the contract’s existence. The company has the right to refuse such business when it is presented, but once the business is accepted, the company waives the right to deny coverage on the basis of denial of acceptance.

General Agent Duties to Insurers

Because of the law of agency, there are various general obligations an insurance agent may owe to an insurance carrier, which differ, depending upon the carrier,

the following are general duties to consider:

• fiduciary duty;

• loyalty;

• accounting – collection of premium;

• disclosure of information.

Fiduciary Duty

Where a high level of trust arises in connection with the insurance agent- principal relationship, it can be considered to be a fiduciary one. Often fiduciary relationships involve the handling of money.

Loyalty

The agent has the duty of loyalty to its principal. The duty of loyalty embraces several subsidiary obligations, including :

• refraining from competing with the principal;

• taking action on behalf of or otherwise assisting the principals competitors;

• not acquiring a material benefit from a third party in connection with actions taken through the agents use of the agents position;

• not using or communicating confidential information of the principal for the agents own purposes or those of a third party.

Accounting – Collection of Premium

In general, the premiums due on a new insurance transaction are collected by the producer and checks are made out by the customer to the agency, and then owed to the carrier (less any commission due).

These net premiums may be held for a period of time before the agency turns them over to the carrier in accordance with the terms of the agency agreement.

Disclosure of Information

Since the agent is representing the principal, and since the agent’s knowledge is imputed to the principal, it is reasonable for the principal to expect that their agent will provide them with any material information of which the agent is aware .

Agreement between the insurer and the agent setting out the details of the appointment of the agent, duties, documentation, remuneration etc.

Agreement between Insurer and Agent

This is a written contract stipulating the arrangement between an insurance agency and the insurer it represents. Important details such as ownership of renewals, commission percentages, and duties and responsibilities of each party are usually spelled out in this agreement.

Insurance agents have contractual agreements (known as Appointments) with insurers that set up the guidelines for the policies they can offer and the terms of their remuneration. A ‘captive agent’ is an agent dedicated to one insurance company’s product while an 'independent agent'can align themselves with multiple insurers. The insurance agent therefore aims to attract insurance business for their principal(s).

Insurance is sold primarily by agents. The underlying contract, therefore, is affected significantly by the legal authority of the agent, which in turn is determined by well-established general legal rules regarding agency. The law of agency basically deals with the legal consequences of people acting on behalf of other people or organizations.

Agency involves three parties: the principal, the agent, and a third party. The principal(insurer) creates an agency relationship with a second party by authorizing him or her to make contracts with third parties (policyholders) on the principal’s behalf. The second party to this relationship is known as the agent, who is authorized to make contracts with a third party. It is important to note the difference between an agent who represents the insurer and a broker who represents the insured. However, in certain instances brokers are not allowed to operate unless they also obtain an agency appointment with an insurer.

The source of the agent’s authority is the principal. Such authority may be either expressed or implied. When an agent is appointed, the principal is required to expressly indicate the extent of the agent’s authority in the agreement. The agent also has, by implication, whatever authority is needed to fulfil the purposes of the agency.

By entering into the relationship, the principal implies that the agent has the authority to fulfil the principal’s responsibilities, implying apparent authority. From the public’s point of view, the agent’s authority is whatever it appears to be.

If the principal treats a second party as if the person were an agent, then an agency is created. When entering to such agreements the parties should be aware that agency law and the doctrines of waiver and estoppel have serious implications in the insurance business.

Binding Authority

The law of agency is significant to insurance in large part because the only direct interaction most buyers of insurance have with the insurance company is through an agent or a broker, also called a producer. Laws regarding the authority and responsibility of an agent, therefore, affect the contractual relationship.

One of the most important agency characteristics is binding authority. In many situations, an agent is able to exercise binding authority, which secures (binds) coverage for an insured without any additional input from the insurer. The agreement that exists before a contract is issued is called a binder. This arrangement, described in the offer and acceptance section, is common in the property/casualty insurance areas. If you call an agent in the middle of the night to obtain insurance for your new motor vehicle, you are covered as of the time of your conversation with the agent.

In life and health insurance, an agent’s ability to secure coverage is generally more limited. Rather than issuing a general binder of coverage, some life insurance agents may be permitted to issue only a conditional binder. A conditional binder implies that coverage exists only if the underwriter ultimately accepts (or would have accepted) the application for insurance. Thus, if the applicant dies prior to the final policy issuance, payment is made if the applicant would have been acceptable to the insurer as an insured. The general binder, in contrast, provides coverage immediately, even if the applicant is later found to be an unacceptable policyholder and coverage is cancelled at that point.

Estoppel

Estoppel occurs when the insurer or its agent has led the insured into believing that coverage exists and, as a consequence, the insurer cannot later claim that no coverage existed. For example, when an insured specifically requests a certain kind of coverage when applying for insurance and is not told it is not available, that coverage likely exists, even if the policy wording states otherwise, because the agent implied such coverage at the time of sale, and the insurer is estopped from denying it.

Agency by Estoppel

An agency relationship may be created by estoppel when the conduct of the principal implies that an agency exists. In such a case, the principal will be estopped from denying the existence of the agency (recall the binding authority of some agents). This situation may arise when the company suspends an agent, but the agent retains possession of blank policies.

People who are not agents of a company do not have blank policies in their possession. By leaving them with the former agent, the company is acting as if he or she is a current agent. If the former agent issues those policies, the company is estopped from denying the existence of an agency relationship and will be bound by the policy.

If an agent who has been suspended sends business to the company that is accepted, the agency relationship will be ratified by such action and the company will be estopped from denying the contract’s existence. The company has the right to refuse such business when it is presented, but once the business is accepted, the company waives the right to deny coverage on the basis of denial of acceptance.

General Agent Duties to Insurers

Because of the law of agency, there are various general obligations an insurance agent may owe to an insurance carrier, which differ, depending upon the carrier,

the following are general duties to consider:

• fiduciary duty;

• loyalty;

• accounting – collection of premium;

• disclosure of information.

Fiduciary Duty

Where a high level of trust arises in connection with the insurance agent- principal relationship, it can be considered to be a fiduciary one. Often fiduciary relationships involve the handling of money.

Loyalty

The agent has the duty of loyalty to its principal. The duty of loyalty embraces several subsidiary obligations, including :

• refraining from competing with the principal;

• taking action on behalf of or otherwise assisting the principals competitors;

• not acquiring a material benefit from a third party in connection with actions taken through the agents use of the agents position;

• not using or communicating confidential information of the principal for the agents own purposes or those of a third party.

Accounting – Collection of Premium

In general, the premiums due on a new insurance transaction are collected by the producer and checks are made out by the customer to the agency, and then owed to the carrier (less any commission due).

These net premiums may be held for a period of time before the agency turns them over to the carrier in accordance with the terms of the agency agreement.

Disclosure of Information

Since the agent is representing the principal, and since the agent’s knowledge is imputed to the principal, it is reasonable for the principal to expect that their agent will provide them with any material information of which the agent is aware .

Legal App FREE Download - We Handle Your Case On The Go