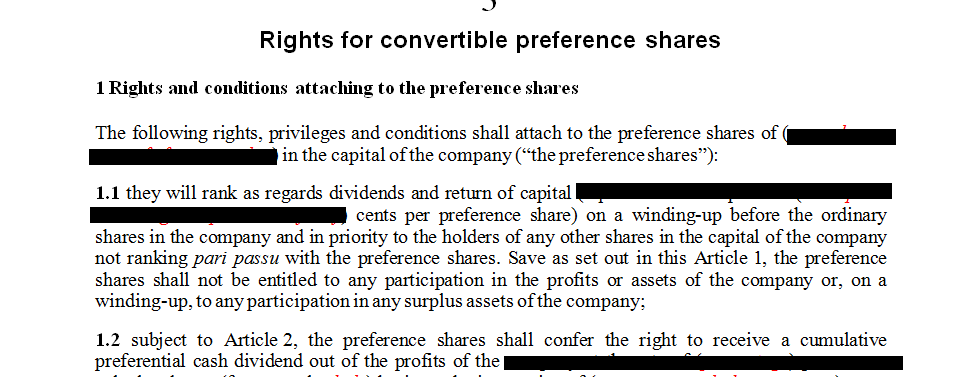

Rights for convertible preference shares

FREE

Ask the similar questions

Rights for convertible preference shares

The Companies Act and preference shares

The Companies Act (Act 71 of 2008) regulates the authorisation and issue of the various classes of shares by a company, including preference shares.

With regard to shares in general, and preference shares in particular, the following regulations in the Companies Act are, among other things, noteworthy:

• Chapter 2, Part D, Section 35 (1)

A share issued by a company is moveable property, transferable in any manner provided for or recognised by this Act or other legislation.

• Chapter 2, Part D, Section 35 (3)

A company may not issue shares to itself.

• Chapter 2, Part D, Section 35 (4)

An authorised share of a company has no rights associated with it until it has been issued.

• Chapter 2, Part D, Section 36 (1)

A company’s Memorandum of Incorporation:

• must set out the classes of shares, and the number of shares of each class, that the company is authorised to issue;

• must set out, with respect to each class of shares:

(i) distinguishing designation for that class; and

(ii) the preferences, rights, limitations, and other terms associated with that class, subject to paragraph (d);

• may set out a class of shares:

(ii) for which the board of the company must determine the associated preferences, rights, limitations, or other terms, and

• (iii) which must not be issued until the board of the company has determined the associated preferences, rights, limitations, or other terms, as contemplated in subparagraph (ii).

• Chapter 2, Part D, Section 36 (2)

The authorisation and classification of shares, the numbers of authorised shares of each class, and the preferences, rights, limitations and other terms associated with each class of shares, as set out in a company’s Memorandum of Incorporation, may be changed only by –

• an amendment of the Memorandum of Incorporation by special resolution of the shareholders; or

• the board of the company, in the manner contemplated in subsection (3), except to the extent that the Memorandum of Incorporation provides otherwise.

• Chapter 2, Part D, Section 36 (3)

Except to the extent that a company’s Memorandum of Incorporation provides otherwise, the company’s board may –

• increase or decrease the number of authorised shares of any class of shares;

• reclassify any classified shares that have been authorised but not issued.

What is a Convertible Preferred Stock?

Convertible preferred stocks are preferred shares that include an option for the holder to convert the shares into a fixed number of common shares after a predetermined date. Most convertible preferred stock is exchanged at the request of the shareholder, but sometimes there is a provision that allows the company, or issuer, to force conversion.

The value of a convertible preferred stock is ultimately based on the performance of the common stock.

Key Considerations

• Convertible preferred shares can be converted into common stock at a fixed conversion ratio.

• Once the common share moves above the conversion price, it may be worthwhile for the preferred shareholders to covert and realize an immediate profit.

• After a preferred shareholder converts their shares, they give up their rights as a preferred shareholder (no fixed dividend or higher claim on assets) and become a common shareholder (ability to vote and participate in share price declines and rises).

Understanding Convertible Preferred Stock

Convertible preferred stock is used by corporations for fundraising purposes. Companies can raise capital in two ways: debt or equity. Debt must be paid back regardless of the firm's financial situation, but it generally costs less to obtain after tax incentives.

Equity gives up ownership but does not need to be paid back. Both forms of capital fundraising have their advantages and disadvantages. Preferred shares are a type of hybrid security, falling somewhere between debt and equity.

Equity gives shareholders ownership, which gives them voting rights, but they have little claim on assets if the company falters and liquidates.

This is because debt holders and preferred stockholders are paid out prior to common shareholders from any assets remaining. Preferred stock is a hybrid security that gives the shareholder a fixed dividend and a claim on assets if the company liquidates.

In exchange, preferred shareholders don't have voting rights like common shareholder do.

Preferred and common stock will trades at different prices due to their structural differences. Preferred stocks aren't as volatile and resemble a fixed income security.

There are many different types of preferred securities including cumulative preferred, callable preferred, participating preferred, and convertibles. Convertible preferred stock provides investors with an option to participate in common stock price appreciation.

Preferred shareholders receive an almost guaranteed dividend. However, dividends for preferred shareholders do not grow at the same rate as they do for common shareholders. In bad times, preferred shareholders are covered, but in good times, they do not benefit from increased dividends or share price. This is the trade-off.

Convertible preferred stock provides a solution to this problem. In exchange for a typically lower dividend (compared to non-convertible preferred shares), convertible preferred stock gives shareholders the ability to participate in share price appreciation.

Convertible preferred stock can be converted to common shares at the conversion ratio. The conversion ratio is set by the company before the preferred stock is issued. For example, one preferred stock may be converted into two, three, four, and so on, common shares.

If the common shares rise, the preferred shareholder may opt to convert their shares into common stock, thus realizing an immediate profit. The price at which converting becomes profitable for the investor is called the conversion price.

The Companies Act (Act 71 of 2008) regulates the authorisation and issue of the various classes of shares by a company, including preference shares.

With regard to shares in general, and preference shares in particular, the following regulations in the Companies Act are, among other things, noteworthy:

• Chapter 2, Part D, Section 35 (1)

A share issued by a company is moveable property, transferable in any manner provided for or recognised by this Act or other legislation.

• Chapter 2, Part D, Section 35 (3)

A company may not issue shares to itself.

• Chapter 2, Part D, Section 35 (4)

An authorised share of a company has no rights associated with it until it has been issued.

• Chapter 2, Part D, Section 36 (1)

A company’s Memorandum of Incorporation:

• must set out the classes of shares, and the number of shares of each class, that the company is authorised to issue;

• must set out, with respect to each class of shares:

(i) distinguishing designation for that class; and

(ii) the preferences, rights, limitations, and other terms associated with that class, subject to paragraph (d);

• may set out a class of shares:

(ii) for which the board of the company must determine the associated preferences, rights, limitations, or other terms, and

• (iii) which must not be issued until the board of the company has determined the associated preferences, rights, limitations, or other terms, as contemplated in subparagraph (ii).

• Chapter 2, Part D, Section 36 (2)

The authorisation and classification of shares, the numbers of authorised shares of each class, and the preferences, rights, limitations and other terms associated with each class of shares, as set out in a company’s Memorandum of Incorporation, may be changed only by –

• an amendment of the Memorandum of Incorporation by special resolution of the shareholders; or

• the board of the company, in the manner contemplated in subsection (3), except to the extent that the Memorandum of Incorporation provides otherwise.

• Chapter 2, Part D, Section 36 (3)

Except to the extent that a company’s Memorandum of Incorporation provides otherwise, the company’s board may –

• increase or decrease the number of authorised shares of any class of shares;

• reclassify any classified shares that have been authorised but not issued.

What is a Convertible Preferred Stock?

Convertible preferred stocks are preferred shares that include an option for the holder to convert the shares into a fixed number of common shares after a predetermined date. Most convertible preferred stock is exchanged at the request of the shareholder, but sometimes there is a provision that allows the company, or issuer, to force conversion.

The value of a convertible preferred stock is ultimately based on the performance of the common stock.

Key Considerations

• Convertible preferred shares can be converted into common stock at a fixed conversion ratio.

• Once the common share moves above the conversion price, it may be worthwhile for the preferred shareholders to covert and realize an immediate profit.

• After a preferred shareholder converts their shares, they give up their rights as a preferred shareholder (no fixed dividend or higher claim on assets) and become a common shareholder (ability to vote and participate in share price declines and rises).

Understanding Convertible Preferred Stock

Convertible preferred stock is used by corporations for fundraising purposes. Companies can raise capital in two ways: debt or equity. Debt must be paid back regardless of the firm's financial situation, but it generally costs less to obtain after tax incentives.

Equity gives up ownership but does not need to be paid back. Both forms of capital fundraising have their advantages and disadvantages. Preferred shares are a type of hybrid security, falling somewhere between debt and equity.

Equity gives shareholders ownership, which gives them voting rights, but they have little claim on assets if the company falters and liquidates.

This is because debt holders and preferred stockholders are paid out prior to common shareholders from any assets remaining. Preferred stock is a hybrid security that gives the shareholder a fixed dividend and a claim on assets if the company liquidates.

In exchange, preferred shareholders don't have voting rights like common shareholder do.

Preferred and common stock will trades at different prices due to their structural differences. Preferred stocks aren't as volatile and resemble a fixed income security.

There are many different types of preferred securities including cumulative preferred, callable preferred, participating preferred, and convertibles. Convertible preferred stock provides investors with an option to participate in common stock price appreciation.

Preferred shareholders receive an almost guaranteed dividend. However, dividends for preferred shareholders do not grow at the same rate as they do for common shareholders. In bad times, preferred shareholders are covered, but in good times, they do not benefit from increased dividends or share price. This is the trade-off.

Convertible preferred stock provides a solution to this problem. In exchange for a typically lower dividend (compared to non-convertible preferred shares), convertible preferred stock gives shareholders the ability to participate in share price appreciation.

Convertible preferred stock can be converted to common shares at the conversion ratio. The conversion ratio is set by the company before the preferred stock is issued. For example, one preferred stock may be converted into two, three, four, and so on, common shares.

If the common shares rise, the preferred shareholder may opt to convert their shares into common stock, thus realizing an immediate profit. The price at which converting becomes profitable for the investor is called the conversion price.

Legal App FREE Download - We Handle Your Case On The Go