Certificate for options

FREE

Ask the similar questions

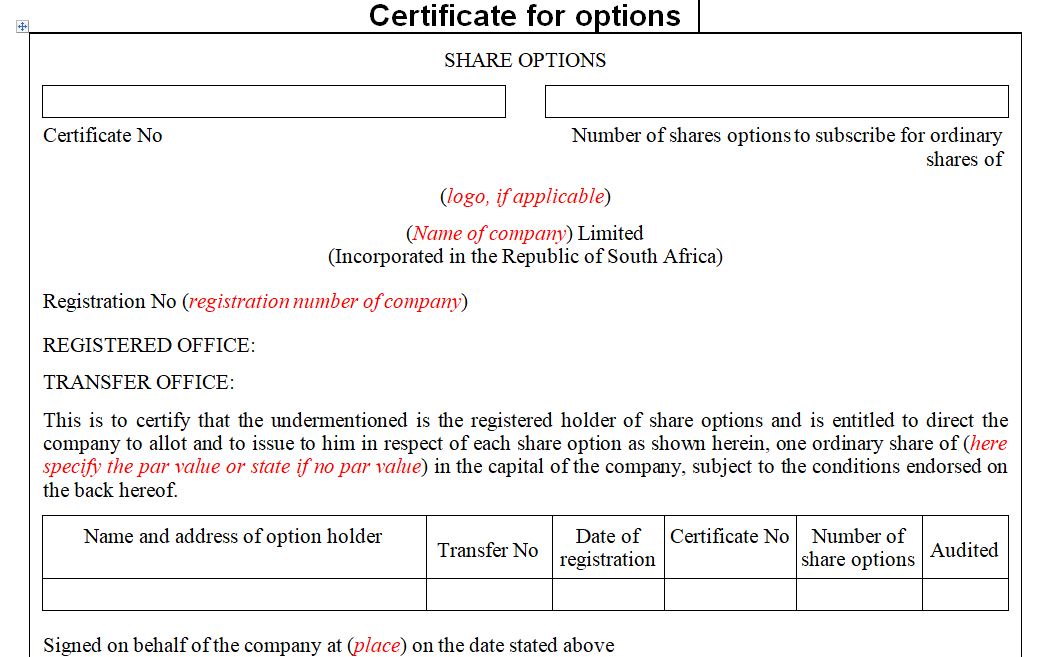

Certificate for options

Certificate for Options

With an employee stock option plan, you are offered the right to buy a specific number of shares of company stock, at a specified price called the grant price (also called the exercise price or strike price), within a specified number of years.

Your options will have a vesting date and an expiration date. You cannot exercise your options before the vesting date or after the expiration date.

Your options are considered to be “in the money” when the current market price of the stock is greater than the grant price.

Below is a summary of the terminology you will see in your employee stock option plan:

• Grant price/exercise price/strike price – the specified price at which your employee stock option plan says you can purchase the stock;

• Issue date – the date the option is given to you;

• Market price – the current price of the stock;

• Vesting date - the date you can exercise your options according to the terms of your employee stock option plan;

• Exercise date – the date you do exercise your options;

• Expiration date – the date by which you must exercise your options or they will expire.

Types of Options

There are two types of stock options companies issue to their employees:

• NQs – Non-Qualified Stock Options;

• ISOs – Incentive Stock Options.

Different tax rules apply to each type of option. With non-qualified employee stock options, taxes are most often withheld from your proceeds at the time you exercise your options. This is not necessarily the case for incentive stock options. With proper tax planning, you can minimize the tax impact of exercising your options.

Your employee stock option plan will have a plan document that spells out the rules that apply to your options. Get a copy of this plan document and read it, or hire a financial planner that is familiar with these types of plans to assist you.

There are many factors to consider in deciding when to exercise your options. Investment risk, tax planning, and market volatility are a few of them, but the most important factor is your personal financial circumstances, which may be different than those of your co-worker.

It is important to keep the following in mind before following anyone’s advice:

Should You Keep the Stock?

Keeping too much company stock is considered risky. When your income and a large portion of your net worth is all dependent on one company if something bad happens to the company your future financial security could be in jeopardy. Corporate executives need to consider this in their planning and work to diversify out of company stock.

Company Share Option Plans (“CSOP”)

The CSOP is a tax qualified discretionary option plan under which a company may grant options to any employee or full-time director to acquire shares at an exercise price which must be not less than the market value of the shares on the grant date. The exercise is generally tax relieved allowing gains to be taxed as capital on the sale of the shares.

Conditions

In order to qualify for beneficial tax treatment, a Company Share Option Plans (CSOP) must meet requirements in respect of:

• eligibility of individuals to participate;

• shares which may be subject to option;

• limits; and

• self-certification.

Eligible Employees

Options may be granted on a discretionary basis to any employee or any full-time director of the establishing company (or any constituent company in the case of a group plan).

If the establishing company is a close corporation, participants are ineligible if they (or their associates) have (or have had within the previous 12 months) a "material interest" (broadly 30% of the ordinary share capital or assets) in the company.

Plan Shares

Plan shares must be fully paid up, non-redeemable, ordinary shares which are:

• in an independent company; or

• listed on a recognised stock exchange.

Plan shares qualify if there is only one class of shares in issue. If there is more than one class in issue, the majority of shares of the same class as plan shares must be either "employee-control" shares or "open market" shares. Shares will be employee control shares if employees and directors (and former employees and former directors) control the company by virtue of holding shares of the same class as plan shares.

Shares will be open market shares if (broadly) the majority of shares of the same class as plan shares are not held by persons who acquired them by reason of their employment or directorships (or by trustees who hold such shares on their behalf).

Since 17 July 2013 plan shares may be subject to restrictions so, for example, it is possible for unlisted companies to require CSOP option- holders to enter into a power of attorney which allows the attorney to exercise the option and to sell the option shares on their behalf should an exit be achieved.

With an employee stock option plan, you are offered the right to buy a specific number of shares of company stock, at a specified price called the grant price (also called the exercise price or strike price), within a specified number of years.

Your options will have a vesting date and an expiration date. You cannot exercise your options before the vesting date or after the expiration date.

Your options are considered to be “in the money” when the current market price of the stock is greater than the grant price.

Below is a summary of the terminology you will see in your employee stock option plan:

• Grant price/exercise price/strike price – the specified price at which your employee stock option plan says you can purchase the stock;

• Issue date – the date the option is given to you;

• Market price – the current price of the stock;

• Vesting date - the date you can exercise your options according to the terms of your employee stock option plan;

• Exercise date – the date you do exercise your options;

• Expiration date – the date by which you must exercise your options or they will expire.

Types of Options

There are two types of stock options companies issue to their employees:

• NQs – Non-Qualified Stock Options;

• ISOs – Incentive Stock Options.

Different tax rules apply to each type of option. With non-qualified employee stock options, taxes are most often withheld from your proceeds at the time you exercise your options. This is not necessarily the case for incentive stock options. With proper tax planning, you can minimize the tax impact of exercising your options.

Your employee stock option plan will have a plan document that spells out the rules that apply to your options. Get a copy of this plan document and read it, or hire a financial planner that is familiar with these types of plans to assist you.

There are many factors to consider in deciding when to exercise your options. Investment risk, tax planning, and market volatility are a few of them, but the most important factor is your personal financial circumstances, which may be different than those of your co-worker.

It is important to keep the following in mind before following anyone’s advice:

Should You Keep the Stock?

Keeping too much company stock is considered risky. When your income and a large portion of your net worth is all dependent on one company if something bad happens to the company your future financial security could be in jeopardy. Corporate executives need to consider this in their planning and work to diversify out of company stock.

Company Share Option Plans (“CSOP”)

The CSOP is a tax qualified discretionary option plan under which a company may grant options to any employee or full-time director to acquire shares at an exercise price which must be not less than the market value of the shares on the grant date. The exercise is generally tax relieved allowing gains to be taxed as capital on the sale of the shares.

Conditions

In order to qualify for beneficial tax treatment, a Company Share Option Plans (CSOP) must meet requirements in respect of:

• eligibility of individuals to participate;

• shares which may be subject to option;

• limits; and

• self-certification.

Eligible Employees

Options may be granted on a discretionary basis to any employee or any full-time director of the establishing company (or any constituent company in the case of a group plan).

If the establishing company is a close corporation, participants are ineligible if they (or their associates) have (or have had within the previous 12 months) a "material interest" (broadly 30% of the ordinary share capital or assets) in the company.

Plan Shares

Plan shares must be fully paid up, non-redeemable, ordinary shares which are:

• in an independent company; or

• listed on a recognised stock exchange.

Plan shares qualify if there is only one class of shares in issue. If there is more than one class in issue, the majority of shares of the same class as plan shares must be either "employee-control" shares or "open market" shares. Shares will be employee control shares if employees and directors (and former employees and former directors) control the company by virtue of holding shares of the same class as plan shares.

Shares will be open market shares if (broadly) the majority of shares of the same class as plan shares are not held by persons who acquired them by reason of their employment or directorships (or by trustees who hold such shares on their behalf).

Since 17 July 2013 plan shares may be subject to restrictions so, for example, it is possible for unlisted companies to require CSOP option- holders to enter into a power of attorney which allows the attorney to exercise the option and to sell the option shares on their behalf should an exit be achieved.

Legal App FREE Download - We Handle Your Case On The Go